Great Expectations

Children like stories and so do investors. The latest story, which has captured the imagination of investor community, is, ‘a stable government will unlock the growth potential of India.’

This story has, in part, restored investors’ faith, which was thrashed, when the ‘decoupled from developed nations’ story failed to stand up to their expectations.

What investor community doesn’t realize, however, is that just as children stories are fictitious; these stories can be fictitious, inspite of them sounding realistic. And, as a famous philosopher, once observed, ‘“we're never so vulnerable than when we trust someone,’ investors’ end up being a vulnerable lot.

The behavior of investors, at large, can be likened to a balloon. The more inflated it is with optimism, the more vulnerable it is to blow up in the face of slightest trouble.

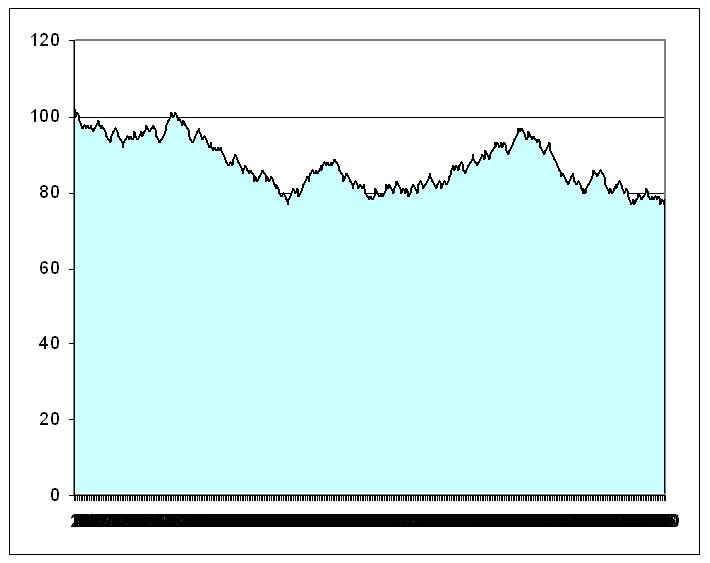

The historic rally, which we have witnessed during this week, highlights the tendency of investors to take a good story too far. Of course, it is a relief, more than anything else that we have a stable government after numerous elections resulting in hung parliament halting economic reforms.

But, as Benjamin Franklin observed, ‘he who pays in advance gets a penny worth for a nickel paid,’ investors, in their optimism, always seem to end up paying in advance (think, forward earnings estimate to justify the high valuations of stocks) and end up disappointed (as earnings fail to catch up with expectations and PE multiples collapse).

The SENSEX closed at 13,887 on May 22nd, 2009. This discounts the earnings at19x. Given the cloud of uncertainty prevailing world over and dipping industrial production levels, such an earnings multiple seem to contain elements of irrational exuberance.

At PPFAS, we are not in the business of making market predictions and neither is this a prediction that markets are ripe for correction or over-valued. After all, there is a lot of wisdom in John Maynard Keynes’ advice, ‘markets can remain irrational for longer than you can remain solvent.’

The purpose of this article is to highlight the manic depressive behavior that market displays every now and then and how susceptible, in the process, it becomes to disappointment. And in markets, disappointments mean losing not only one’s hard-earned savings but also losing one’s sleep.

Let me end the article with an excellent quote from Benjamin Graham, which sums up the essence of the whole article succinctly and is, to some extent a reply to the ‘unlocking of growth potential of India’ story,

‘Obvious prospects for physical growth in a business do not translate into obvious profits for investors.’

This story has, in part, restored investors’ faith, which was thrashed, when the ‘decoupled from developed nations’ story failed to stand up to their expectations.

What investor community doesn’t realize, however, is that just as children stories are fictitious; these stories can be fictitious, inspite of them sounding realistic. And, as a famous philosopher, once observed, ‘“we're never so vulnerable than when we trust someone,’ investors’ end up being a vulnerable lot.

The behavior of investors, at large, can be likened to a balloon. The more inflated it is with optimism, the more vulnerable it is to blow up in the face of slightest trouble.

The historic rally, which we have witnessed during this week, highlights the tendency of investors to take a good story too far. Of course, it is a relief, more than anything else that we have a stable government after numerous elections resulting in hung parliament halting economic reforms.

But, as Benjamin Franklin observed, ‘he who pays in advance gets a penny worth for a nickel paid,’ investors, in their optimism, always seem to end up paying in advance (think, forward earnings estimate to justify the high valuations of stocks) and end up disappointed (as earnings fail to catch up with expectations and PE multiples collapse).

The SENSEX closed at 13,887 on May 22nd, 2009. This discounts the earnings at19x. Given the cloud of uncertainty prevailing world over and dipping industrial production levels, such an earnings multiple seem to contain elements of irrational exuberance.

At PPFAS, we are not in the business of making market predictions and neither is this a prediction that markets are ripe for correction or over-valued. After all, there is a lot of wisdom in John Maynard Keynes’ advice, ‘markets can remain irrational for longer than you can remain solvent.’

The purpose of this article is to highlight the manic depressive behavior that market displays every now and then and how susceptible, in the process, it becomes to disappointment. And in markets, disappointments mean losing not only one’s hard-earned savings but also losing one’s sleep.

Let me end the article with an excellent quote from Benjamin Graham, which sums up the essence of the whole article succinctly and is, to some extent a reply to the ‘unlocking of growth potential of India’ story,

‘Obvious prospects for physical growth in a business do not translate into obvious profits for investors.’

posted by Arpit Ranka at 12:36 PM

3 comments

![]()

![]()